When a brand-name drug’s patent expires, the first generic company to file a challenge gets a 180-day window to sell its version without competition. This isn’t just a head start-it’s a financial lifeline. During those six months, that first generic captures 70 to 80% of the market, selling at 70-90% of the original brand price. That’s how they pay back the $5-10 million they spent fighting the patent in court. But once that clock runs out, everything changes. Suddenly, competitors flood in. And prices don’t just drop-they collapse.

Why the second generic hits harder than the first

The first generic might get the spotlight, but the second one is what really breaks the market. When only one generic is available, prices hover around 83% of the brand’s cost. Add a second, and that drops to 66%. But when the third one arrives? Prices plunge to 49%. That 25-30% drop between the second and third entrant is the steepest in the entire cycle. By the time five or more generics are on the shelf, the drug often sells for just 17% of the original price. Take Crestor, the cholesterol drug. When its patent expired in 2016, the brand sold for $320 a month. Within 18 months, eight generic makers were selling it. The price? $10 a month. That’s not a discount-it’s a demolition.Authorized generics: the brand’s secret weapon

Here’s where it gets tricky. The brand company doesn’t just sit back and watch. Many launch their own version-called an authorized generic-right when the first generic hits the market. These aren’t knockoffs. They’re made by the same company, under the same name, sometimes even in the same factory. But they’re sold at generic prices. In 2019, Merck did this with Januvia, a diabetes drug. On the exact day the first generic launched, Merck rolled out its own authorized version through a subsidiary. Within six months, it grabbed 32% of the market. The first generic’s share dropped from 80% to 40-50%. Revenue for the first entrant? Cut by 30-40%. This tactic is common: 65% of big-brand drugs launch authorized generics during the 180-day exclusivity period. It’s legal. It’s strategic. And it’s devastating for the first mover.Who enters next-and how they do it

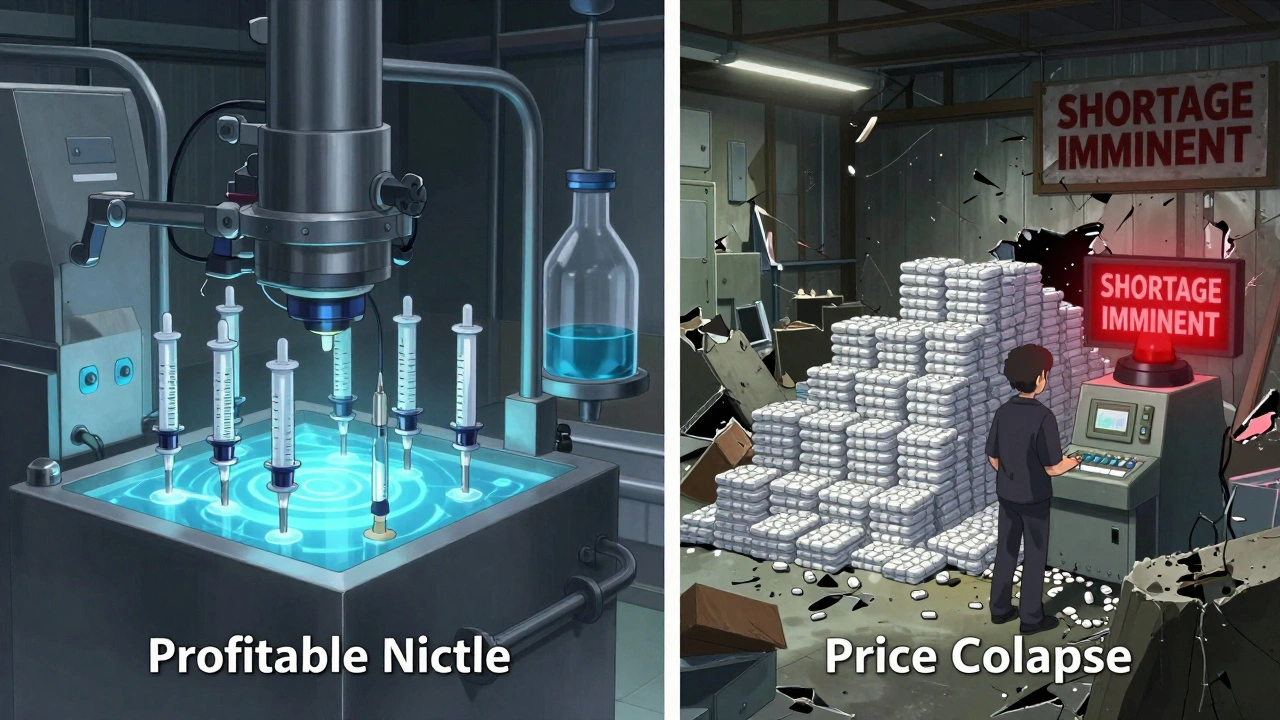

Companies waiting to enter after the first generic don’t just copy and paste. They’re playing a long game. They watch the court rulings, track the first entrant’s supply chain, and wait for the right moment. Some time their launch to avoid direct competition. Others rush in as soon as the exclusivity ends, betting on volume. They also rely heavily on contract manufacturers. While the first generic often builds its own production line, 78% of second-and-later entrants outsource manufacturing. It saves money-$5 million in upfront costs-but it creates a new risk: quality control. The FDA found that 62% of generic shortages involve drugs with three or more manufacturers. Why? Because the same contract plant is making pills for five different companies. One bad batch, one inspection failure, and everyone’s supply gets disrupted.

The hidden battle: PBMs and formulary placement

Getting FDA approval is only half the fight. The real battle happens behind closed doors with pharmacy benefit managers (PBMs). These companies control which drugs get covered by insurance plans. And they don’t care who got approved first. They care who offers the lowest price. In 2023, 68% of PBM contracts used a "winner-take-all" model. That means only one generic gets placed on the formulary-and it’s usually the one that bids the lowest, not the one that entered first. So even if you’re the second or third generic to hit the market, if you offer a better deal, you can lock up 80-90% of sales. This creates a "second first-mover advantage." It’s not about timing anymore. It’s about pricing power.Patent games and delays

Brand companies don’t give up easily. After the first generic enters, they file what’s called "citizen petitions"-requests to the FDA to delay approval of others. Between 2018 and 2022, there were 1,247 of these petitions. Each one slows down the next competitor by an average of 8.3 months. That’s a long time when you’re trying to get into a market that’s already losing 10-15% in price with every new entrant. Some patent fights end in settlements. In the case of Humira, six biosimilar makers agreed to stagger their entry between 2023 and 2025. No rush. No price war. Just controlled, scheduled competition. These deals are legal, and they’re becoming more common. They protect the brand’s revenue-and hurt the generics’ ability to build momentum.

15 Comments

i just found out my mom's cholesterol med went from $400 to $12 a month and i cried. like, how is this even legal? we're saving lives but barely scraping by.

this is wild. the first generic gets all the glory but gets crushed by the second one. it's like winning a race only to get hit by a truck right after the finish line.

so the brand companies just... make their own generics? genius. i mean, if you can't beat 'em, join 'em and then pretend you're still the boss.

the PBM winner-take-all model is pure oligopoly theater. they're not optimizing for patient access-they're optimizing for margin compression. it's a race to the bottom with corporate middlemen holding the ladder.

i mean... someone has to pay for all this innovation, right? if we just let generics destroy prices, who's gonna fund the next breakthrough drug? we're eating the seed corn here.

I've seen this firsthand: contract manufacturers making pills for five different companies. One fails an FDA audit, and suddenly, half the country can't get their blood pressure med. It's not a supply chain-it's a house of cards.

this is all a psyop. the pharma giants own the FDA, the PBMs, the courts. they let one generic in so they can control the price collapse. it's not capitalism-it's a scripted performance.

i spent 14 hours last night reading about this because i have a kid with epilepsy and we're one bad batch away from disaster. i can't sleep. i can't breathe. they don't care. nobody cares. it's just pills. just numbers. just profit.

the authorized generic move is so sneaky it’s almost impressive. like, you paid millions to fight the patent, then the brand just drops their own version for half the price. you’re not outcompeted-you’re outmaneuvered.

i live in a rural town. when the third generic for metformin hit, the pharmacy stopped stocking it because the profit was less than the cost of the shelf space. we had to drive 40 miles. this isn’t a market-it’s a minefield.

i love how the system rewards the slowest player. the first mover gets crushed, the second gets squeezed, but the one who waits 18 months and underbids everyone? they win. it’s like a video game where you lose if you rush.

Let me just say, as someone who actually studied pharmaceutical economics at a tier-one institution, this entire system is a grotesque failure of incentive alignment. The FDA’s approval process is not designed for scale, and PBMs are unregulated monopolists masquerading as cost-containment agents. The fact that we allow contract manufacturing for life-saving drugs without mandatory quality audits is not just negligent-it’s morally indefensible. We are literally gambling with human lives on the back of shareholder value. And yet, we praise ‘market efficiency’? What a joke.

the complex generics are where the real innovation is now-patches, inhalers, injectables. it’s not sexy, but someone’s gotta make them. and honestly? i’d rather have two reliable makers than ten that vanish after a recall.

so the first guy spends $10 million to break the patent, then gets gutted by the brand’s own fake generic, then the next five companies all outsource to the same sketchy factory in India, and now no one can get their meds because one guy had a bad batch? i think we just invented the world’s most expensive game of Jenga.

this is the invisible architecture of modern healthcare: profit decay curves, patent cliffs, formulary gatekeepers. we treat drugs like commodities, but they’re not. they’re lifelines. and we’ve turned the market into a desert where the first to arrive gets the last drop.

Write a comment