Ever signed a massive stack of papers at the doctor's office without really looking at them? Most of us do. We assume it's just standard bureaucracy, but those forms often hide the difference between a manageable medical bill and a financial nightmare. For years, healthcare providers could bundle your consent for treatment and your agreement to pay into one single signature. That's essentially like signing a contract to buy a car while you're still deciding if you even want to drive it.

Things are changing, especially in places like New York, where consumer protection laws are finally catching up to the reality of medical debt. With millions of people facing collections over health costs, the legal landscape is shifting to stop predatory financial practices before they start. Whether you're dealing with a surprise bill from an out-of-network specialist or trying to figure out why your clinic wants your credit card on file before an emergency procedure, there are now specific regulations designed to keep you from being exploited.

Key Protections Against Predatory Medical Billing

One of the biggest traps in modern healthcare is how debt is categorized. When you use a traditional credit card to pay for a surgery, you aren't just borrowing money; you're often converting "medical debt" into "consumer debt." Why does that matter? Because medical debt often has special legal protections-like limits on wage garnishment or liens on your home-that disappear the moment you swipe a Visa or Mastercard.

To fight this, New York introduced General Business Law Section 519-a is a regulation that prohibits healthcare providers from requiring credit card preauthorization or keeping cards on file before providing emergency or medically necessary services . This prevents clinics from "locking in" a high-interest consumer loan before you've even had a chance to negotiate the bill or check your insurance coverage.

Additionally, providers are now required to be honest about the risks. They can't just suggest a credit card; they must inform you that paying with traditional credit strips away the federal and state protections that usually apply to healthcare-specific financing. It's a critical distinction that can save a patient from bankruptcy if a treatment doesn't go as planned.

The Fight Against "Bundled" Consent

For decades, the "all-in-one" intake form was the industry standard. You signed one piece of paper, and suddenly you had consented to the medical procedure and agreed to all the provider's payment terms. This lack of transparency left many patients blindsided by the costs of their care.

Public Health Law Section 18-c is a mandate requiring healthcare providers to obtain separate, distinct patient consent for treatment and for payment . This means if a clinic wants your permission to treat you and your agreement to their payment plan, they need two different signatures. While there has been some confusion regarding its enforcement-with reports of temporary suspensions in 2025-the intent is clear: you should never be forced to agree to a financial arrangement just to get the medical care you need.

Stopping Provider Interference in Financing

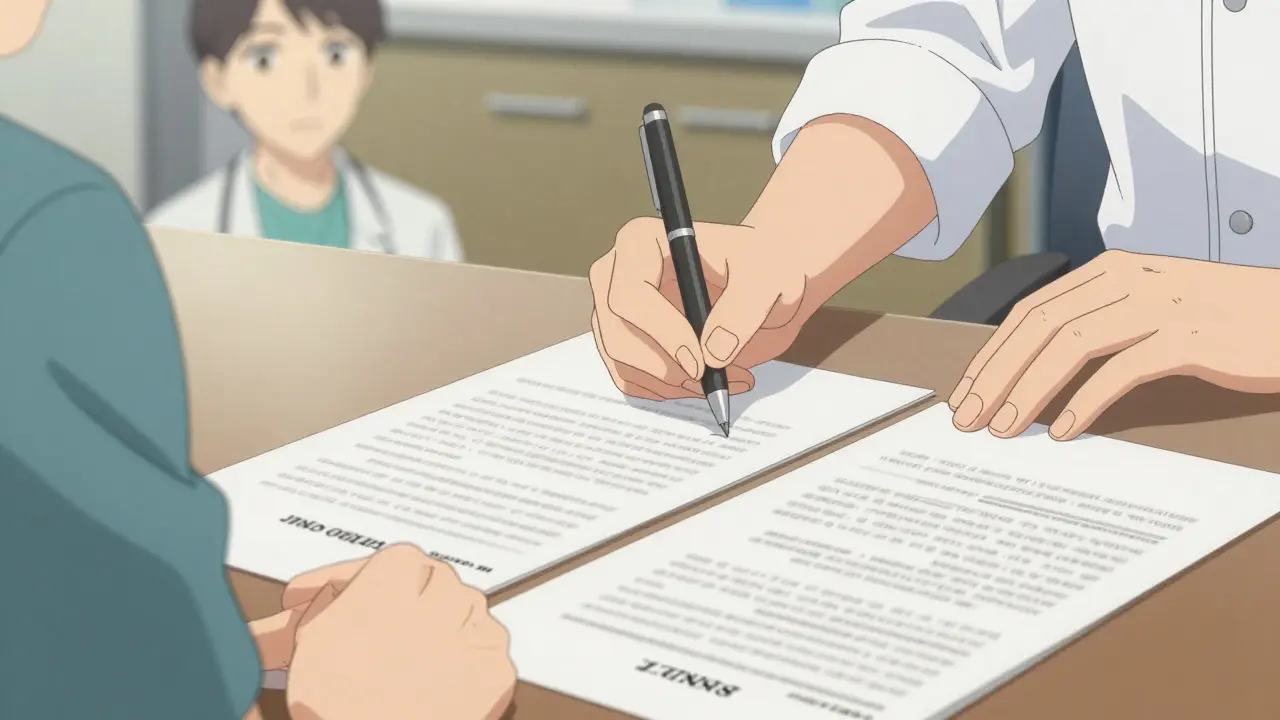

Have you ever had a receptionist offer to "help" you fill out an application for a medical loan? It might seem friendly, but it can be a conflict of interest. Some providers prefer certain financing products because they get better terms or faster payouts, even if those products are worse for the patient.

To curb this, General Business Law Section 349-g is a law that prohibits healthcare providers from completing any portion of a patient's application for medical financial products . If you're applying for something like CareCredit®, the provider can answer your questions, but they cannot touch the pen or type into the form for you. This ensures the patient is the one making the financial commitment, not a staff member trying to hit a quota or speed up the intake process.

| Protection Type | Federal (e.g., No Surprises Act) | New York State Laws | Primary Benefit |

|---|---|---|---|

| Surprise Billing | Strong (Out-of-network) | Strong | Stops unexpected bills from unknown doctors. |

| Payment Consent | General | Strict (Separate Forms) | Decouples care from financial agreements. |

| Credit Card Pre-auth | Minimal | Prohibited for Emergencies | Prevents forced consumer debt. |

| Application Assistance | Not regulated | Prohibited | Ensures patient-led financial decisions. |

Understanding the Federal Safety Net

While state laws provide a sharper edge, federal regulations create the foundation. The No Surprises Act is a federal law effective since January 1, 2022, that protects patients from unexpected medical bills when they receive emergency care or certain non-emergency care from out-of-network providers . This law was a response to the "balance billing" nightmare where a patient goes to an in-network hospital, but the anesthesiologist happens to be out-of-network, resulting in a bill for thousands of dollars.

Then there is the HIPAA (Health Insurance Portability and Accountability Act), which governs how your health information is shared. While we often think of HIPAA in terms of privacy, it's a crucial part of consumer protection because it prevents your medical data from being leaked to debt collectors or employers without your explicit permission.

Moreover, the Consumer Financial Protection Bureau (CFPB) has stepped in to address the long-term impact of medical debt. In 2024, the CFPB finalized a rule to remove medical bills from credit reports. This is a massive win for patients because it prevents a single health crisis from destroying your credit score for a decade.

Red Flags: When to Question Your Provider

Knowing the law is great, but recognizing a violation in real-time is where the real value lies. If you encounter these scenarios, you should pause and ask for clarification:

- The "Combo" Form: If you're asked to sign one document that covers both your medical consent and your financial responsibility, ask for separate forms.

- The "Helpful" Clerk: If a staff member starts filling out your financing application for you, politely ask them to stop and finish it yourself.

- The Pre-Auth Demand: If a clinic refuses to treat an emergency unless you put a credit card on file for "guaranteed payment," they may be violating state-specific emergency care laws.

- The Credit Card Push: If a provider suggests using a standard credit card over a medical-specific loan without explaining that you'll lose medical debt protections, ask why they aren't mentioning the risks.

How to Handle a Dispute

If you feel these laws have been ignored, don't just pay the bill and hope for the best. Start by requesting an itemized bill. Many providers will magically find "errors" that lower the price once they know you're tracking the details. If the provider has violated consent laws-like using a bundled form-you may have leverage to negotiate the total cost.

For serious violations, especially those involving predatory financing or denied emergency care, the New York State Department of Health is the primary agency for reporting. Document everything: keep copies of the forms you were asked to sign and the dates of the interactions. If your credit score was impacted by a medical bill that should have been removed under CFPB rules, filing a dispute with the credit bureaus is the most effective path to correction.

What is the difference between a medical financial product and a traditional credit card?

Medical financial products (like specialized health loans) often come with legal protections that keep the debt classified as "medical." This can protect your primary residence from liens and limit how debt collectors can garnish your wages. Traditional credit cards convert this into "consumer debt," which gives creditors more power to seize assets or report the debt to credit agencies more aggressively.

Can a doctor's office still help me with my financing application?

Yes, they can answer your questions and provide general assistance. However, under laws like NY General Business Law Section 349-g, they cannot actually fill out any part of the application for you. You must be the one to physically or digitally complete the form to ensure the decision is yours and not influenced by the provider.

Does the No Surprises Act cover every medical bill?

No. It primarily protects you from "surprise" bills resulting from emergency services or from out-of-network providers who work at an in-network facility. It does not cover bills for services you explicitly agreed to receive from an out-of-network provider after signing a waiver.

What happens if a provider violates the separate consent rule?

In New York, violations of Public Health Law Section 18-c can lead to fines of up to $2,000 per incident. While the patient doesn't get the fine, this creates a strong incentive for providers to fix their paperwork processes and respect patient autonomy.

Will medical bills still show up on my credit report in 2026?

According to the 2024 CFPB rules, medical bills are being removed from credit reports to prevent health crises from unfairly damaging a person's financial standing. If you see a medical bill on your report, it may be an error or a legacy item that you can now dispute.

14 Comments

Everyone just accepts this garbage because they're too lazy to read the fine print. It's honestly pathetic how people let themselves get robbed by hospitals just because they can't handle a piece of paper. You basically hand over your life savings and then act shocked when the bill hits. This is just basic financial literacy and most of you fail it miserably. I've always told people to never trust a medical provider with their wallet, but obviously, nobody listens to the guy who actually knows how the system works. It's a joke.

This is such a vital reminder for everyone to be more vigilant about their healthcare documents. I'm particularly interested in how these New York laws might influence other states to adopt similar protections. It seems like a logical progression for consumer rights across the board. We really need to encourage more people to ask for those separate consent forms!

total scam system

Wow... just wow!!! 😱 I had no idea that using a credit card could actually strip away my protections!!! This is so scary but also so important to know... 💖 Let's all try to be kinder to ourselves and more careful with these forms... 🌸✨ Maybe if we all speak up, we can make the whole world's healthcare more human... 🌿🙏

Typical american mess where you need a law just to stop a doctor from stealing your money through a credit card swipe lol this is why we are falling apart as a nation everything is a legal battle now just sign the damn paper and pay for the service like a man

It is truly heartening to see these legislative steps being taken to protect the vulnerable. I believe that with more transparency, the relationship between patients and providers will only improve. This is a wonderful move toward a more ethical healthcare system!

Oh for heaven's sake, the sheer audacity of these clinics to think they can just 'help' you with a loan application is absolutely theatrical! Truly a performance for the ages! I find it utterly exhausting that we live in a society where a receptionist is basically a predatory loan shark in a blazer. It's just so dramatically unfair that I can't even deal with it right now!

I've seen this happen a lot in my professional experience. A great tip is to always ask for the 'chargemaster' list if you're trying to negotiate a bill. Most people don't know it exists, but it's the internal price list hospitals use. Combining that with the No Surprises Act gives you a ton of leverage when fighting an unfair charge. Keep pushing for those itemized bills, guys!

To add to the point about itemized bills, make sure you check for 'upcoding.' This is where a provider bills for a more complex version of the procedure you actually received. If you notice the description on your itemized list doesn't match the care you got, that's a huge red flag. You can actually dispute those specific line items with your insurance company to get the provider to correct the bill.

I'm just so glad that medical bills are being taken off credit reports. I know so many people who are good people but just got hit with one bad accident and their credit was ruined for years. It's a huge relief to know that's changing.

Brilliant breakdown of a very confusing topic. It's a relief to see the CFPB finally stepping in on the credit reporting side of things. A health crisis shouldn't be a financial death sentence.

I totally agree with the point about the 'helpful' clerk. It's such a subtle way to push people into bad deals. We should definitely support these kinds of laws because they empower the patient to make a conscious choice without pressure. Great info here!

the intersection of health and capital is always a tragedy we treat bodies like assets and assets like bodies and these laws are just small band-aids on a systemic collapse

Stay strong everyone. Just take it one step at a time and keep your documents organized. You've got this!

Write a comment